Confronting Capitalism by Philip Kotler is organized around 14 shortcomings. The list is broad and his thinking is brave and deep without being strident or bleak—a daunting challenge and a wonderful contribution given the controversial if not explosive nature of emotions at the intersection of money and politics.

Kotler’s inaugural post for this site invites enhancements to or additions beyond his list. I congratulate him on such openness and submit this post as support for Chapter 5 (Companies Not Covering Their Social Costs). Kotler explains that if air and water pollution results from steel production, then someone bears the cost. If steel companies evade the cost, then it is born by society either through poor health or from the clean up. Chapter 5 does not cover corporate taxes, though, which is a classic way for individuals and companies to cover social costs. If corporations avoid their fair share of the tax burden, then they are not covering their social costs.

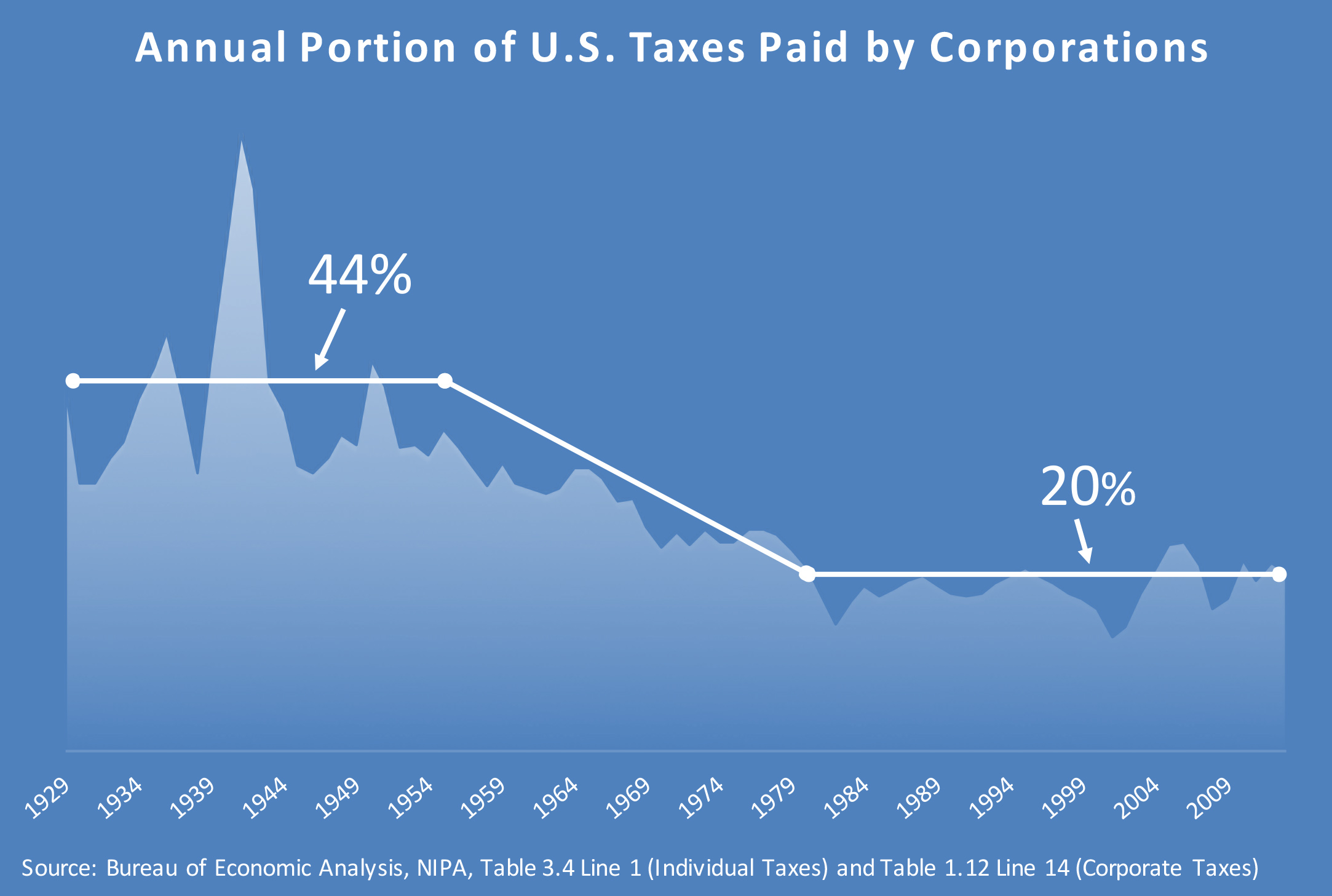

What do we know about corporate taxes relative to social cost?

The bottom line in taxes is: “Who paid what?” Top marginal tax rates don’t really answer this question because they are easily dodged by large corporations and wealthy individuals. We need to measure actual taxes, not marginal rates. As the chart shows, corporations carried 44% of the tax load between 1929 and 1955. The remaining 56% was paid by individuals. Then from 1956 to 1980 the corporate share of taxes dropped precipitously. Since 1981 it leveled out at 20%, and the remaining 80% of the total tax burden has been paid by individuals ever since.

Some might argue that the lower corporate tax burden is appropriate. Perhaps corporations became more socially responsible starting around 1955 and made important non-tax contributions such as enhanced employee programs (e.g., higher employment, compensation, benefits and training)? Maybe they enthusiastically embraced more responsible manufacturing practices (e.g., lower carbon footprint, less natural resource extraction) or better products (e.g., fewer cancer- or obesity-causing products)? Perhaps companies significantly decreased their use of “social goods” (e.g., lower road, bridge and airport use, less need for military intervention or protection)? Or, perhaps their tax burden should have declined due to the rise in social welfare programs?

As Kotler argues throughout his book, it is more reasonable to conclude that companies have radically increased their social costs, not decreased them. They have cut employee programs. They have outsourced work to other countries. They have encouraged consumption of questionable products and aggressively sought legal protections to continue doing so. (Shocking examples of protectionist legislation are found in the meat and dairy industries.) It certainly seems like companies have accelerated their use of public roads, bridges and airports since 1955. U.S. military involvement around the world seems to greatly benefit many powerful U.S. companies. And individual welfare, education and arts programs have suffered extensive defunding and privatization.

Concurrently, corporations dodged their fair share of social costs by investing heavily in lobbying, political spending, tax lawyers and consultants. Indeed, companies now spend more on lobbying than the U.S. spends to fund the House and Senate combined.

Strictly from a shareholder perspective, company efforts to avoid social costs have yielded fabulous returns. Given the pre-1955 proportion of 44%, the decline to 20% yielded a gain of $9 trillion for companies, before considering the time value of money or what they spent on lobbying, political spending, lawyers and consultants. If we add a conservative return to capital of five percent net of costs, then the gain to corporations has been almost $22 trillion. As a point of reference, the market capitalization of the U.S. total stock market is currently about $25 trillion. David Parsley of the Vanderbilt Owen Graduate School of Management and his coauthors studied the return on investment for lobbying expenditures and concluded it was nothing short of dramatic.

From a common citizen’s perspective, the time since 1955 could be described as “The Great Corporate Tax Dodge.” Its cost to society is nearly the value of every publicly traded company in the U.S.

While some deride government ineptitude and insist on further downsizing, the interests of common citizens are better served by empowering government to crack down on corporate tax avoidance and force them to pair their fair share.